BEAR Markets, Speculators in Cryptoassets Lost $2,000,000,000,000 This Year

Dear Friend:

This summer I wanted to write about market volatility and investor behavior in down markets, and then I remembered that we discussed these topics in Noesis’ July 2014 newsletter. Our message is the same now as it was in 2014. Re-reading this newsletter, I realized that I cannot improve our message and that is why we include the July 2014 Noesis letter in this mailing.

Speculators Lose to Cryptoassets

In November 2021, the valuation of all cryptoassets hit a high of approximately $3 trillion. At that time, Bitcoin reached an all-time high of $67,734. However, on June 30, 2022, the value of cryptoassets was $0.9 trillion – down $2.1 trillion from only seven months prior! Bitcoin decreased 72% from its peak and was trading at $18,731. Currently, the S&P 500, NASDAQ, and Russel 1,000 indexes are down 21%, 31%, and 22%, respectively, from their recent highs, and the indexes have gone into Bear market territory.

In the April 2022 Noesis newsletter, we wrote about the decline in the meme stocks: “Meme Stock Hype – a meme stock refers to shares that gain cult-like following through social media platforms.” From the November 2021 high to the June 30, 2022 closing, price shares of Robinhood Markets (-88%), Rivian Automotive (-85%), AMC Entertainment (-77%), Coinbase Global (-87%) and ARK Innovation ETF (-75%) lost in excess of 80% of their values.

The speculators who bought these Meme stocks and/or Bitcoin currencies on margin lost most, if not all, of their investments as many borrowed money to purchase these shares in the first place. These speculators, mostly first-time investors from around the world, wiped out their savings and were possibly left with negative cash balances on their accounts. Consequently, they had to sell the shares of good-quality companies to make up for the losses and to pay for higher living expenses like rent, food and fuel prices. The losses in Meme stocks and cryptocurrencies, and the stock sale to cover the margins, together created enormous selling pressure.

Uncertain Headlines

The headline news has not been good this year with Covid’s Omicron variant, food and fuel shortages, high inflation, rising interest rates, supply chain bottlenecks at U.S. ports, labor shortages, fear of recession, Covid lockdowns in China, Russian-Ukrainian conflict, and political issues. This news has made investors understandably concerned and nervous.

The good news has been mostly ignored by the media and by investors: unemployment numbers are at historical lows, the balance of cash and cash equivalents in U.S. households is at an all-time high of $18.5 trillion and the companies in your portfolios have strong balance sheets and cash flows. These companies are even buying back their own shares; for example, Nike announced an $18 billion stock buyback last month.

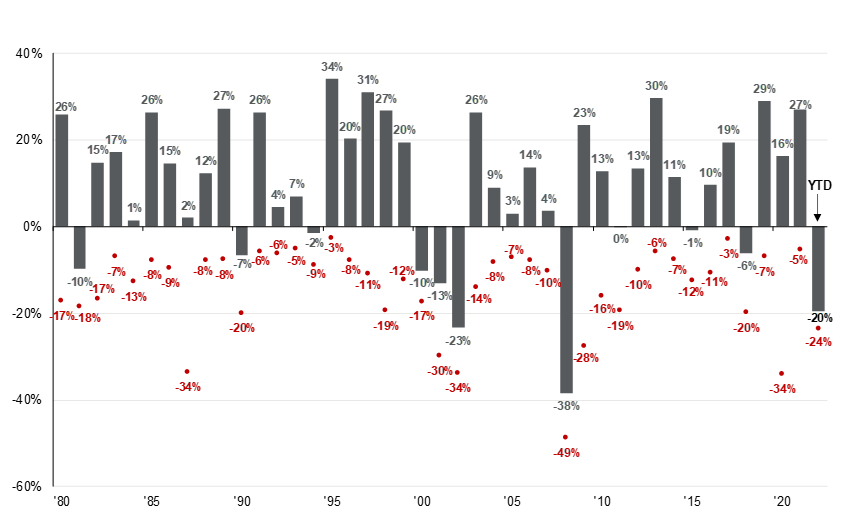

Annual Returns and Intra-Year Declines

The chart below from J.P. Morgan shows that volatility is not unusual for the stock market. The average intra-year drop has been 14% since 1980. However, the market has positively returned more than two-thirds of the time (red numbers show the intra-year declines, and black numbers are the annual returns).

Source: Dalbar, JP Morgan Asset Management

In 2020, the stock market went down 34% from its high when Covid locked down global economies and the world came to a standstill. However, the index closed up 16% for the year.

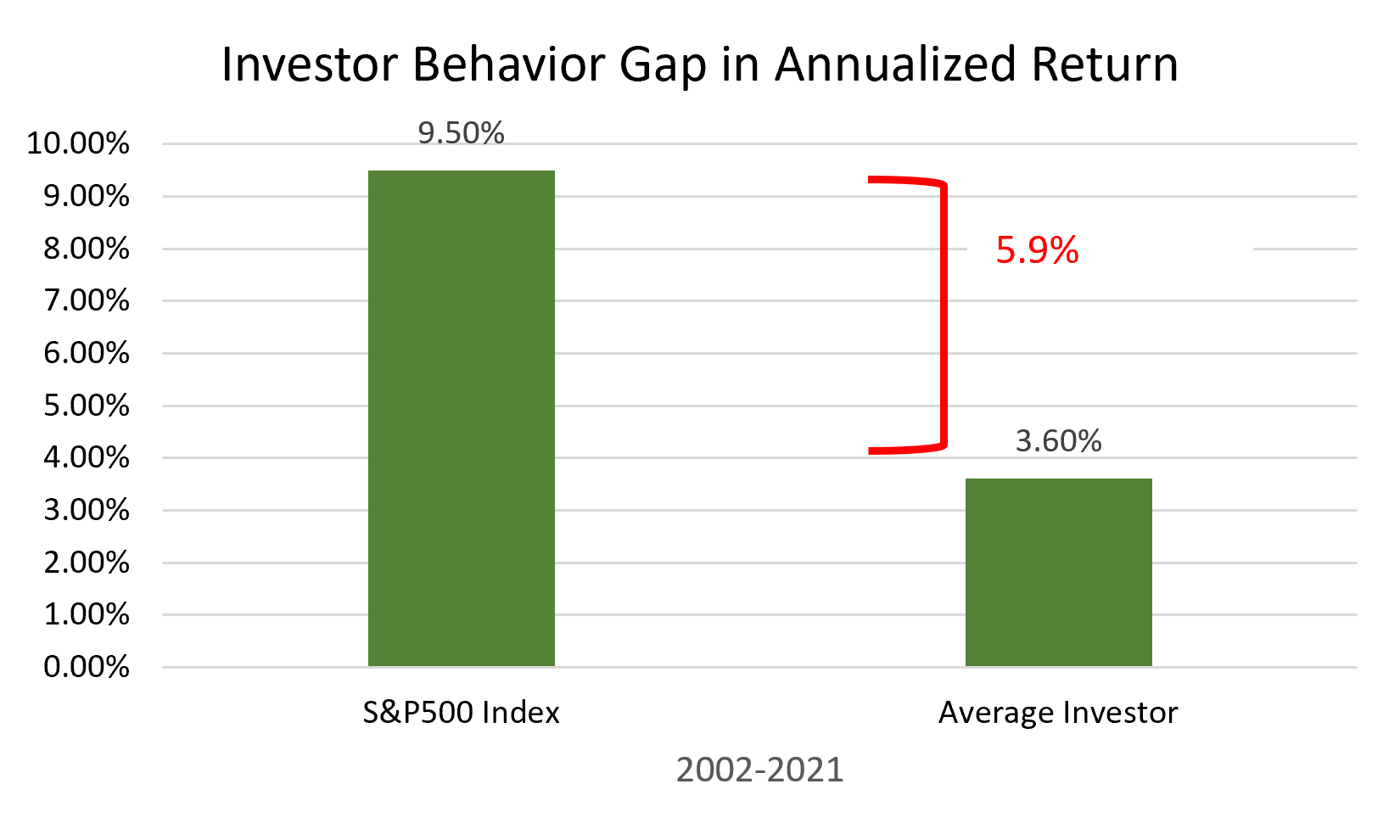

Average Investor Underperformed due to Irrational Behavior

Below is an updated chart on the investor behavior gap that we discussed in 2014. It has been eight years since we first wrote about investor behavior and its impact on portfolio performance for the average equity fund investor. Unfortunately, we continue to see a deterioration of the performance gap over the years. In 2014, it was an annualized gap of 4.2% from 1995 to 2014, and the gap widened to 5.9% from 2002 to 2021. Multiple significant events occurred in both periods, but investor behavior hasn’t changed much. If $1 million were to be invested in 2002, the rational investors who stayed invested during the market volatility would have generated $4.1 million more than the average equity fund investors in 20 years.

Source: Dalbar, JP Morgan Asset Management

Conclusion

Markets have corrections very often. As one client/friend said, “I have seen this rodeo many times before.” However, how should investors behave in down markets?

The message is clear: down markets lower the value of good quality companies, and these stocks become more attractive, not less. Most recessions last only a couple of quarters, and historically markets go up and bounce back in the middle of a recession when the headline news is still negative. Banks in the U.S. passed the stress test at the end of June 2022 and we don’t expect a severe recession as banks, consumers and corporate balance sheets are strong. In short, a mild and short-lived recession creates buying opportunities.

I want to thank all of our clients, partners, and friends: through every down cycle, you have shown that you and your families are rational investors who stick with our proven investment philosophy and stay disciplined. The cumulative returns have shown that this investment approach has served Noesis clients since our founding almost 30 years ago – and a lot has happened in the last 30 years. Our continuous objective is to bring financial peace of mind to the families we serve. Thank you for your trust and friendship, enjoy the summer, and please feel free to forward our current and 2014 newsletters to family members and friends (2014 newsletter: https://www.noesis-capital.com/2nd-quarter-2014/).

Sincerely yours,

Nico Letschert, CFP®