Opportunities Through Market Volatilities

Dear Friend:

As we are approaching the last quarter of 2021, we face many issues: the continuing pandemic, inflation, supply chain disruption, labor shortage, elevated government debt burden, China growth deceleration, and less predictable weather patterns. Almost every segment of society – the business communities, governments, healthcare professionals, and environmentalists – are all trying to figure out the next best actions. It might appear to be the worst of times, but it could also be the best of times in terms of turning these challenges into opportunities.

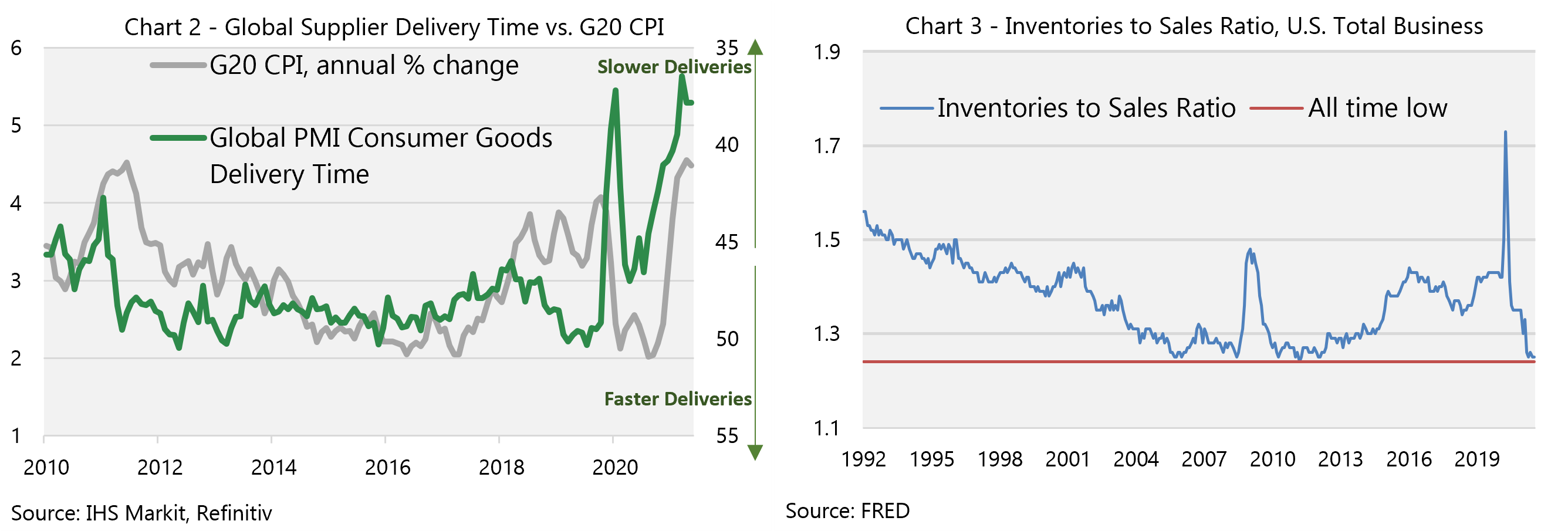

Supply chain disruption was the most alarming issue when factories and ports were closed during the pandemic. Protective gear and things needed to support a work-from-home environment are manufactured in Asia and shipped to the West by container ships. Chart 1 shows how much the container ship freight cost for China departures has increased since the pandemic. In the beginning, even the export countries had to stop shipping essential medical supplies and drug ingredients overseas. Chart 2 shows the prolonged delivery times and the pricing pressures caused by the delay. For decades, the global supply chain and just-in-time manufacturing have left a slim buffer for extreme shocks in supply or demand. Chart 3 shows that the inventories to sales ratio of U.S. total business is at the lowest for the past 30 years. This issue poses many security concerns. It forces the import countries, especially the U.S., to reconsider their manufacturing footprint, a result from pursuing the lowest marginal cost and avoiding strict environmental regulations.

Chart 2 shows the prolonged delivery times and the pricing pressures caused by the delay. For decades, the global supply chain and just-in-time manufacturing have left a slim buffer for extreme shocks in supply or demand. Chart 3 shows that the inventories to sales ratio of U.S. total business is at the lowest for the past 30 years. This issue poses many security concerns. It forces the import countries, especially the U.S., to reconsider their manufacturing footprint, a result from pursuing the lowest marginal cost and avoiding strict environmental regulations.

The worst disruption is the shortage of semiconductor supplies because chips are widely used in industrial and technology products. For example, several automakers in the U.S., Japan, and Germany had to shut down their factories, and for a while, certain used cars were priced higher than new ones. Remapping the semiconductor manufacturing locations is difficult due to immense capital requirements, usually in the tens of billion dollars for a new plant, and the high percentage of skilled workers with science degrees needed. Most semiconductor companies run a fabless model, which means they design the chips but outsource the production to foundries. Only a few, like Intel and Texas Instruments, have the capability of producing chips in-house. Even Intel must outsource its most advanced chips to foundries to achieve a better manufacturing yield.

One of our holdings, Taiwan Semiconductor Manufacturing (TSM), is the pioneer of semiconductor foundry industry. With its core competence in producing smaller-sized chips with lower power consumption and faster processing speed, TSM holds the enabling technology of the smartphone, cloud computing, artificial intelligence, and machine learning industries. TSM was running at total capacity during the pandemic, thanks to the clean-room environment and the well-controlled COVID situation in Taiwan. TSM plans to build new factories in the U.S. and expand in Japan and Europe to address the supply chain issues. Such endeavors are capital intensive and will impact profitability in the short term; however, these projects are necessary and should be long-term accretive since they will address the security concern on the supply chain and diversify the geopolitical risk from Taiwan.

Linde PLC, a global industrial gas provider, has signed a long-term agreement with a foundry partner to supply ultra-high-purity nitrogen, oxygen, and argon to a multi-billion-dollar new facility in Arizona. Linde will build, own, and operate a complex of on-site plants designed to meet the most stringent requirements of the semiconductor industry and maintain world-class reliability and operating efficiency. With Linde’s worldwide reach and reputation, the remap of foundry’s footprint will bring Linde ample and sustainable opportunities in the coming years.

Amphenol, a producer of electronic connectors, sensors, and antennas, is another company that benefited from supply chain issues due to its flexible operation model, distributed manufacturing capacity, and localized decision-making strategy. Amphenol has approximately 125 general managers with near full autonomy, so it can quickly meet clients’ demand through product redesign and alternative sourcing during the current supply chain crunch. Since Amphenol uses relatively low semiconductor content, it can supply customers continuously and gained market share during the pandemic.

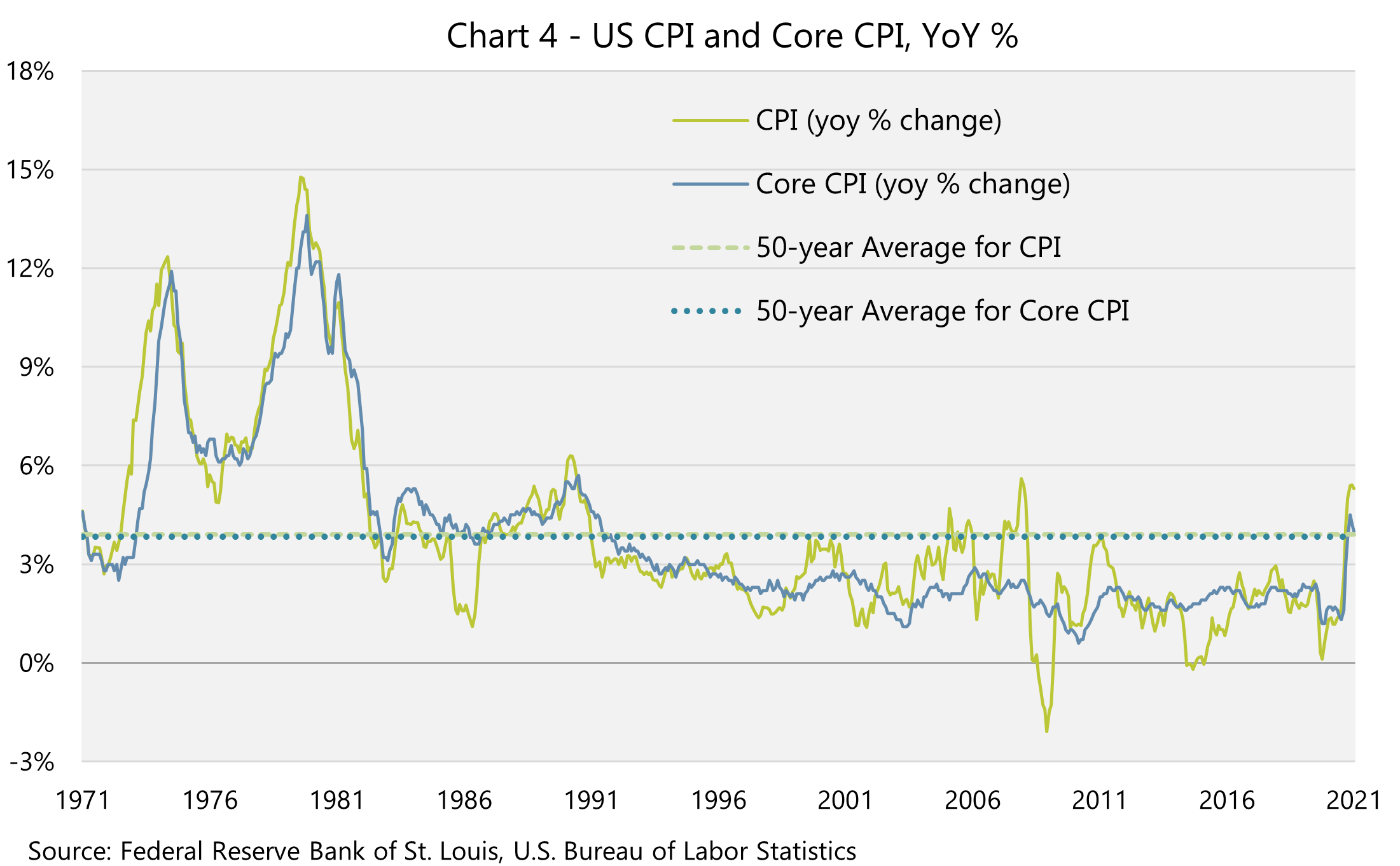

The disruption to the global supply chain we described earlier is one reason for the elevated inflation we witness in the U.S. (chart 4) and globally (chart 2). Labor shortage, partly driven by increased unemployment benefits, and pent-up demand, are others. In addition, we compare this year’s higher price levels to very low levels during the pandemic outbreak in 2020, the so-called base effect. Despite the Federal Reserve’s assertion that this surge in inflation is transitory and related to the economic reopening, some causes might prove to be longer-lasting.

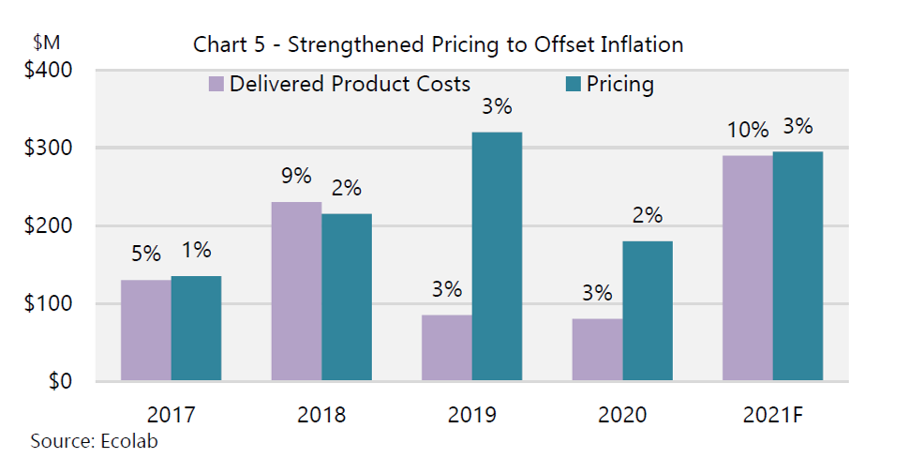

Companies in good market positions can offset cost inflation with pricing power. For example, Ecolab announced a 4% price increase in the second half of 2021 to offset rising input costs. The 4% is a firmwide average with higher increases in its industrial segment. Chart 5 demonstrates Ecolab’s ability to pass inflation pressure to its customers in past years.

A good forecast and procurement plan can mitigate the inventory bottleneck and input cost pressure. Lowe’s mentioned during its latest earnings call that they ordered seasonal merchandise for Halloween and Christmas earlier than usual, foreseeing supply-chain constraints. Orders for holiday merchandise are placed only once a year; thus, timing is crucial. Because they are a large volume customer, Lowe’s was able to leverage its bargaining power with its suppliers.

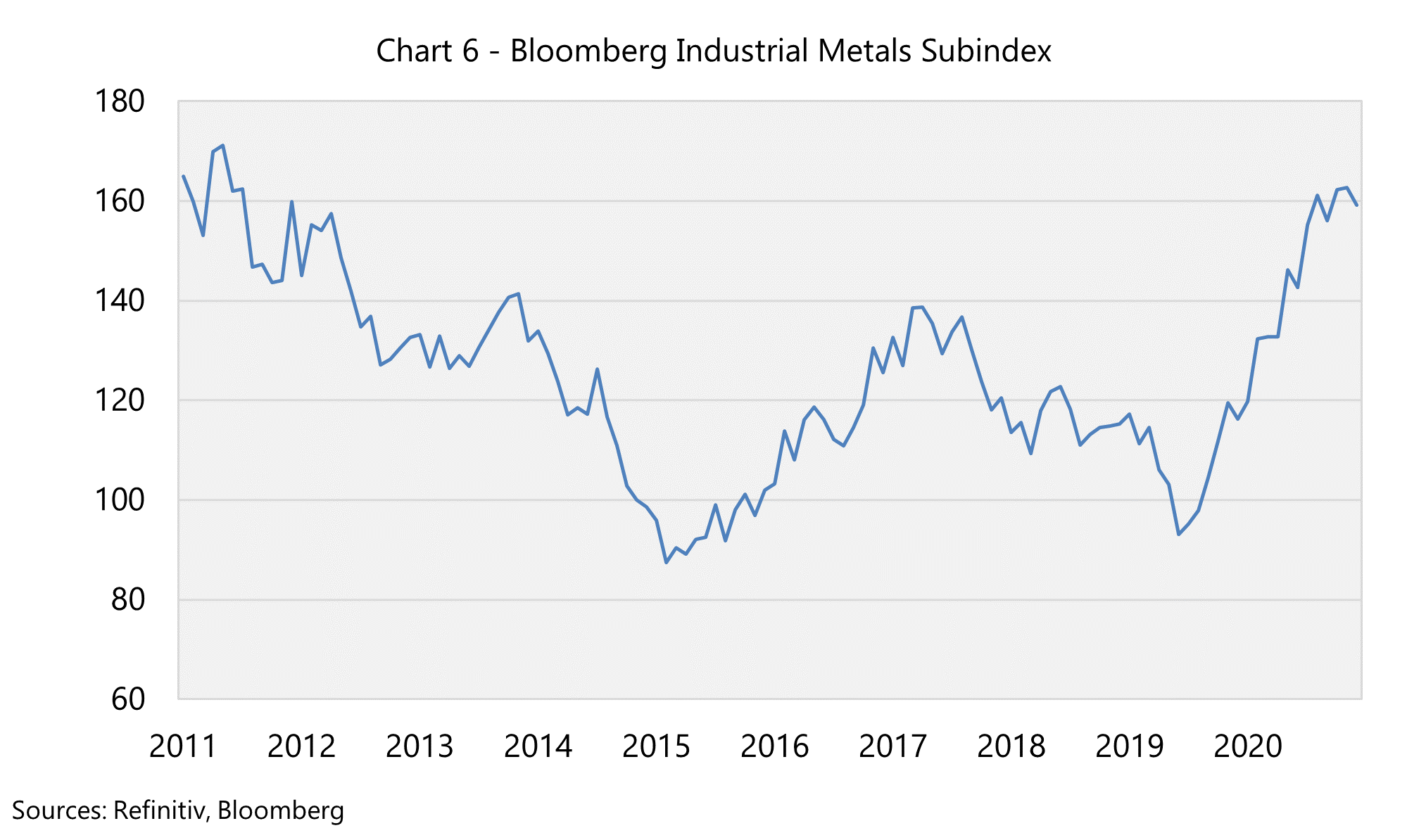

Another example of pricing power is Caterpillar, where management expects to increase prices in the second half of 2021 to offset higher costs from material and freight. Furthermore, industrial metal price inflation (see Chart 6) is a net benefit to Caterpillar’s Mining segment. Higher metal prices translate into increased profit to the mining customers and robust equipment demand to Caterpillar. Management sees a steady improvement in mining capital expenditure reflected in heavy quoting activities and order trends. These stories of Ecolab, Lowe’s, and Caterpillar demonstrate our belief that only those companies with a wide moat protecting the business (in these cases, pricing power) can withstand pressure during unprecedented times.

We mentioned in our January newsletter that we will focus on specific themes, which include the booming middle-class in the emerging markets and online payment. Recently we invested in a Singaporean company, Sea Ltd, which operates an e-commerce platform, online payment, and gaming business in Taiwan, Southeast Asia (Indonesia, Malaysia, Vietnam), Latin America (Brazil, Mexico, Colombia), and recently Poland. According to Bain Capital & Co, Google, Temasek, and Morgan Stanley’s reports, Southeast Asia and Latin America are the most under-penetrated internet economies. The online economy could be three times larger than the current level. Sea’s revenue has grown more than 100 percent per year in the last three years, mainly benefitting from the wealthier middle-class spending more time and money on the internet.

In the e-commerce segment, Sea operates an online shopping platform under the name of Shopee (see picture of Shopee.com’s landing page). It is now the fastest-growing division of the company, and it overtook a competitor to become the most prominent e-commerce operator in the Southeast Asia region. Shopee is the most downloaded shopping app in Latin America despite less than two years of operation. Sea invests in initiatives to help small businesses transact online and benefit from the growth of the digital economy. For instance, it plans to build Shopee centers that serve as regional e-commerce hubs for 5000 villages in West Java, the most populated region in Indonesia and home to around 50 million people. The company expects these centers to provide infrastructure, training, and assistance to help villagers and small businesses to accelerate their digitalization journey.

Sea also offers mobile and P.C. online games in those markets under the division of GARENA. Free Fire, which Sea developed in-house, is now the top-grossing mobile game in Latin America, Southeast Asia, and India. Like the e-commerce and gaming business, Sea’s digital payment product, SeaMoney, also enjoyed robust growth as people spent more time online and shifted to digital payment during the pandemic. Combined with the underbanked situation in those regions, we expect SeaMoney to flourish as well. With Sea, we increased our investment in internet-driven economies. We also have direct exposure to the more affluent consumers in emerging markets other than China.

At Noesis, we take a long-term and bottom-up approach, which requires us to obtain new knowledge, and spot opportunities through market volatilities, externalities, government regulation, and other noise to make sound decisions. There will be inevitable short-term impacts no matter how great these companies are. Our job is to find the best combination of investments that can withstand the impact and deliver results over a long time. Hopefully, these stories can give you peace of mind that our companies remain in good positions during and after the pandemic, as we monitor these challenges closely.

Sincerely yours,

Research Team

Leave A Comment