The Inevitable Slowdown

Dear Friend:

What a summer! It was full of geopolitical events, natural disasters, and an attack on the Middle East oil supply. In the midst of it all, one scenario slowly became apparent – the global economy is weakening. Although we still find data to support a continuous expansion in the U.S. such as the low-interest rate, healthy wage growth, strong consumer spending, and healthy household balance sheets (Chart 1), we also see indicators that predict a decline: the historically low unemployment, plateaued corporate profit growth, and weak capital expenditure (Chart 2). When some aspects of the economy cannot be improved any further, it is natural for the growth engine to slow down. For example, the unemployment rate reached 3.5% in September, the lowest since 1969, and it becomes increasingly difficult to find additional workers. In aggregate, we think a cyclical downturn is in the making, but not necessarily an imminent recession. However, the lack of clarity is hurting business confidence and causing delays in investment.

Chart 1 – Positive data points Chart 2 – Weak or stagnating data points

Weakness was already showing before the trade war intensified in the summer. The tariff dispute has raised the level of uncertainty and is going to hurt consumption and profitability. The impact could be meaningful on both sides of the Pacific. We think China is prepared to fight this trade war for a long time. China’s determination has shown on announced stimulus packages and the accelerated opening of financial markets. It is unlikely that China will agree to a U.S. win-only deal. The truth is – there is no winner in a trade war, and trade is not a zero-sum game; it has to be a win-win situation for both sides to agree.

Globalization and offshoring have indeed left many workers behind, but trade policies are not the only cause for inequality and slow productivity growth. Inadequate tax policies, outdated education systems, and dissatisfactory long-term investments are far more damaging. According to a recent paper by two Harvard University professors, the median household income rose 3% annually between 1948-1973, but only rose 0.4% annually after 1973 in the U.S. Inequality started long before China joined the World Trade Organization in 2001. Similarly, the offshoring of low value-added and high polluting manufacturing capacity cannot be responsible for the weak productivity improvement either. Blindly blaming China for every issue and continuing to ignore the pressing problems only lead to more geopolitical events and hesitation of economic activities and capital investments.

Besides the trade war and warning signs mentioned above, there are other concerns: the impact of coming elections, the negative interest rates, and the friction of Brexit. We don’t usually see so many challenges at the same time. As the uncertainty rises, we need to have proper investments for the downturn. Similar to hurricanes, if we can prepare in advance, we can avoid the worst outcome. In the case of an economic decline, by the time it is confirmed, we would probably be closer to recovery than to the bottom.

We list here the areas of opportunities in preparation for a possible downturn.

- Sustainable growth and early development in a secular trend

We want to own companies that have limited impact from a weak macro-environment since the demand for their unique products and services is unlikely to decline or be challenging to replace. The healthcare sector is one area that should weather the downturn well. We have been overweight in the healthcare sector for a while, and now it has become the anchor of our portfolio. In the information technology sector, we want to own companies whose customers cannot reduce or delay their orders even during a downturn. These products and services are the critical components of future product development or daily operations. For example, in 5G expansion, it takes years to set the standards, to build equipment and infrastructure, and to innovate end products and services. Most of these activities have to continue even during a cyclical downturn. We could say the same things about cloud service providers.

- Strong balance sheet and cash flow

We cannot stress enough how vital a strong balance sheet is in a downturn. In bad times, those with substantial leverage can only watch from the sidelines and see opportunities snatched by others. Those with steady cash flow will be able to procure input material at a lower price and continue to invest, to hire talent, and to take market shares. Companies that can maintain or increase the dividend in difficult times will be regarded as having the highest quality and be added to investors’ portfolios when preference shifts away from pro-growth into risk aversion. The best example was JPMorgan’s acquisition of Bear Stearns for a fire-sale price at the heap of the financial crisis when most of the other banks were fighting for survival.

- Margin expansion

We like companies that can improve margins in a downturn either by improving competitiveness or having cost-cutting plans. During the process of improving margins, companies usually adjust market strategies, right the operations, or optimize the manufacturing footprints and supply chains. Such fine-tunings in a challenging environment often generate a sustainable positive impact on the organizations. Higher margins also give companies leeway to pursue growth once the cycle starts to turn around. Caterpillar, for example, restructured its manufacturing and operation during the commodity price decline in 2015 and was able to expand its margin in the following years.

- Cash and fixed income

We don’t believe we can achieve long-term capital appreciation by timing the market. However, in order to invest when opportunities arise in a downturn, we cannot be powder-dry either. For clients that have a short investment horizon or need income, we still prefer shorter-term income securities even though the current low-rate environment has limited our choices.

What can change all these gloomy predictions and prove our expectations are too pessimistic?

- Decisive monetary policies and large-scale fiscal stimulus

Uncertainty in the monetary policies itself is a negative influence on investment sentiment and spending. Despite the direction of the interest rate movement, we would prefer definite tones from the central banks than ambiguous ones. Fiscal tools can be helpful when the effect of monetary policies is diminishing, and the private sector is reluctant to spend. Most developed countries were leaning toward austerity and debt reduction since the 2008 financial crisis. After decades of neglect, many infrastructure and public projects are due for a big makeover if funding is available. Since passing fiscal stimulus is an easier task in a deteriorating macro environment, we hope to see some countries announcing economic stimulus soon. In Germany, for example, a debate is intensifying to abandon the target of a balanced public household temporarily, borrow at negative interest rates, and invest in technology and green infrastructure.

- A change in the trade war rhetoric

China’s stance is quite clear, and its actions are deliberate and measured. We think the official language is more hawkish than the actions taken. Consistent messages and unyielding leadership are critical to the one-party regime. On the contrary, actions taken by the U.S. seem to be more tactical. Such behavior can change in an instant if the external environment differs. The benefit of a good economy for an incumbent presidential candidate is beyond description. Therefore, we believe there remains a good chance that both sides can agree on a deal, and the declining sentiment can be halted or even turned around.

- China deploys more pro-growth policies

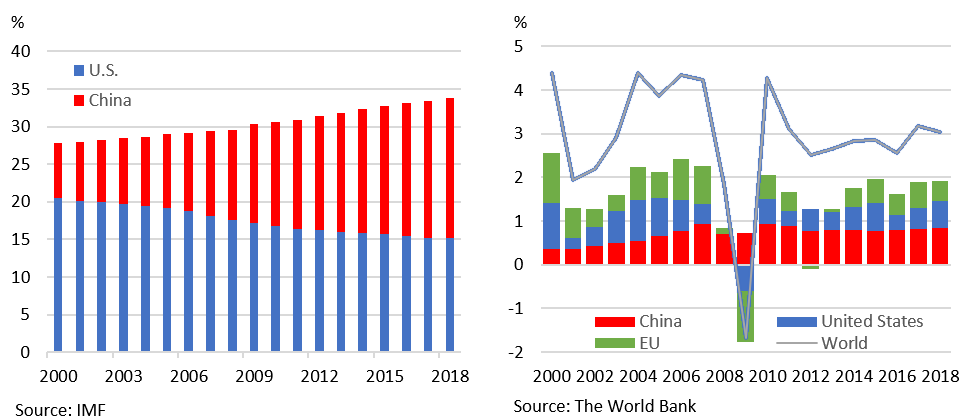

As the world’s second-largest economy growing at twice the global rate, China is the most significant contributor to world GDP growth (see Chart 3 and 4). China is slowing down with or without the trade war after growing at a good pace for three decades. At the same time, structural issues like environment, inequality, and elevated corporate leverage start to impact the growth engine. Fortunately, China still has plenty of stimulus tools. Years of steady growth has created a middle-class larger than the U.S. population. The pro-consumption policies will have a meaningful impact since consumption contributes to over 50% of the economy. If China can keep its growth engine running while other regions are hunkering down, the recovery won’t be too far away. For example, Nike’s revenue in its largest market, North America, grew 4% in the most recent quarter, but the entire company still grew by 10%. The help came from China and other emerging markets, which grew 27% and 13%, respectively.

Chart 3 – Share of world GDP (PPP) Chart 4 – China share of global GDP growth

Even with the proper preparation, no portfolio will work if we don’t invest with a long-term view, or we buy at highs and sell at lows. History has shown that emotional investors are usually too optimistic in bull markets and too pessimistic in bear markets. No one has a crystal ball of the market in such an event-heavy environment, and we should not act according to fear but to rational analysis of the information presenting to us.

For your information

Charles Schwab & Co., Inc., along with most online brokers, very recently announced that they are eliminating trading costs for clients of Noesis, as well as all online trading for all of their clients. This decision further emphasizes the power of the independent model – the Registered Investment Advisor (RIA) that is the foundation of Noesis. Transparency, low cost, excellent execution, independent third-party custodians are all hallmarks of this model. Bernie Clark, Executive Vice President, Schwab Advisor Services, also had this to say:

“For over three decades, we have proudly championed the work of Registered Investment Advisors (RIAs). That is for one reason — we believe in them and what they do.”

As always, we appreciate your business, and please contact us if you have any questions.

Sincerely yours,

Noesis Research Team